The Federal Reserve (Fed) surprised markets over the weekend by holding its March 17-scheduled meeting a few days early and introducing a wide range of provisions. Those provisions are intended to add liquidity, increase credit availability, lower the cost of borrowing, and eventually support the economy’s recovery from the impact of COVID-19.

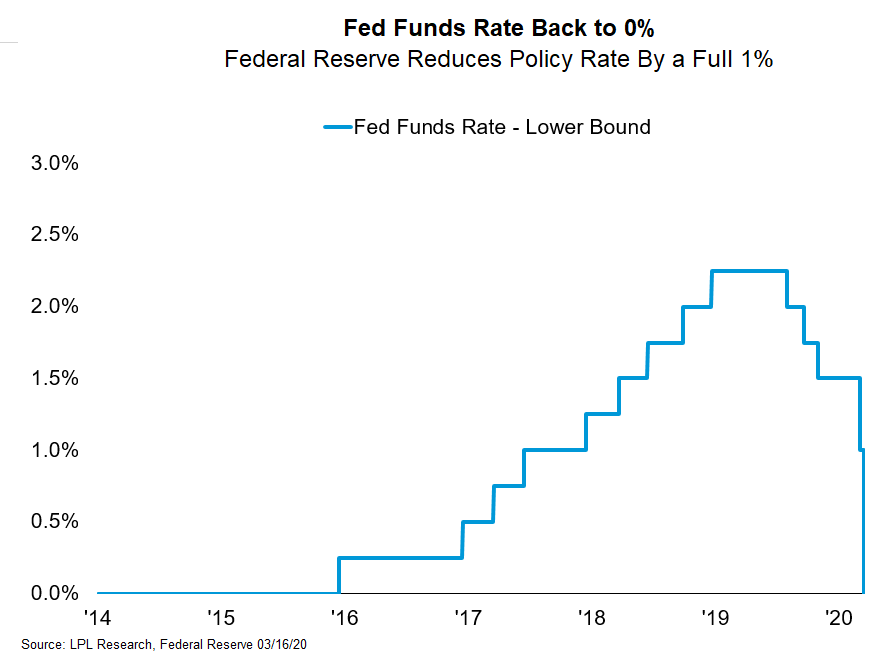

Usually, Fed actions are fundamentally about setting the level of interest rates, and the Fed certainly made a statement there. As shown in our LPL Chart of the Day, the Fed lowered its policy rate a full 1% to a range of 0 – 0.25%, the first time the Fed has made a move that large in a single meeting since the savings and loan crisis of the 1980s. But the policy changes to increase liquidity and relieve funding stress will likely offer a more important short-term impact.

“Lowering borrowing costs probably won’t make a big difference until we move toward recovery and business investment starts to pick up,” said LPL Chief Investment Officer Burt While. “This time around, the Fed’s job was to make sure that a serious global health crisis didn’t turn into a financial crisis by making sure businesses’ short-term funding needs could be met.”

The measures to add liquidity included:

- A new quantitative easing program (QE) in which the Fed committed to buying $700 billion in bonds

- Making it easier for banks to use its discount window, a secondary source of funding

- Working with other central banks to make sure that US dollar demand could be met

- Temporarily reducing bank reserve requirements to zero

Despite the measures, US futures markets were immediately jittery at open Sunday night, quickly falling 5% and hitting the circuit breaker to suspend trading. Market participants were seeing several things. First, while the Fed’s decision to move before the trading week began was prudent, it reinforced to markets that the Fed was starting to see levels of funding stress that it believed had to be addressed as soon as possible. The Fed also unavoidably highlighted the degree of economic uncertainty by declining to provide the economic projections that were scheduled to be released at the March 16–17 meeting, an appropriate move in our view.

With the Fed’s policy rate now at zero, market participants may also be expressing concern that any future policy impact may be limited. Our view is that we may have come to expect too much from the Fed and other central banks. The Fed has always been very good at creating liquidity when needed (the main reason it was created), and has usually been effective at setting rate levels, but it cannot change the underlying fundamental cause of recessions.

The Fed, of course, has no influence over the spread of COVID-19 or the immediate slowdown in economic activity that’s causing. But we believe the Fed stepped up in a big way this weekend and that it will continue to ensure that there is plenty of liquidity to meet short-term funding needs, while also being prepared to support the economy once demand starts to rebound.

IMPORTANT DISCLOSURES

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities. All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

This Research material was prepared by LPL Financial, LLC.

Securities and advisory services offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC).

Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment advice from a separately registered independent investment advisor that is not an LPL affiliate, please note LPL makes no representation with respect to such entity.

If your representative is located at a bank or credit union, please note that the bank/credit union is not registered as a broker-dealer or investment advisor. Registered representatives of LPL may also be employees of the bank/credit union.

These products and services are being offered through LPL or its affiliates, which are separate entities from, and not affiliates of, the bank/credit union. Securities and insurance offered through LPL or its affiliates are:

- Not Insured by FDIC/NCUA or Any Other Government Agency

- Not Bank/Credit Union Guaranteed

- Not Bank/Credit Union Deposits or Obligations

- May Lose Value

For Public Use – Tracking 1-965967