With 20% of S&P 500 Index companies having reported first quarter results so far, earnings season has been a mixed bag. In our April 13 earnings preview, we noted that S&P 500 Index earnings for the quarter were expected to decline 10% year over year, based on FactSet’s consensus estimates from analysts. That number is minus 15% now, largely due to weaker-than-expected results for the financials sector so far. Meanwhile, estimates for the second quarter have fallen from an expected 11% decline on April 1 to a 31% decline as of Thursday, as analysts have updated numbers to factor in what they have learned from companies and to reflect the latest information on stay-at-home orders and business closures.

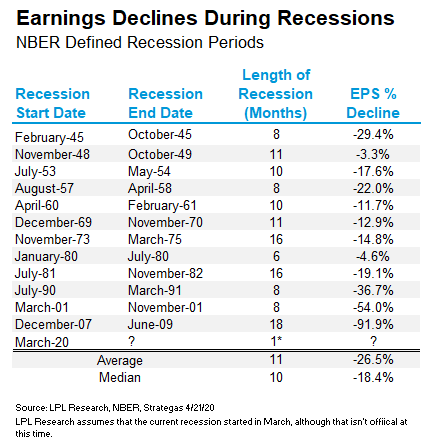

Perhaps the most important question this earnings season is how far might 2020 earnings drop? As shown in the LPL Chart of the Day, thanks to data from our friends at Strategas Research Partners, we can see that drops of 20% or more during recessions are not uncommon.

“Although the average earnings hit has been about 26% historically, the depth of economic contraction we are experiencing suggests the hit could be larger this time,” according to LPL Financial Equity Strategist Jeffrey Buchbinder. “With so many companies pulling guidance and the lack of clarity around the timing of the re-opening of the economy, current consensus estimates calling for a 15% decline in S&P 500 profits this year may prove overly optimistic.”

One reason to think the hit to earnings may not be as bad as some of the worst periods in the accompanying chart is that this recession, while likely severe, will probably be relatively short lived. In addition, when adjusting accounting earnings to get a recurring, operating earnings number, earnings will likely not fall as much (they fell less than 50% during the 2008-2009 financial crisis on this basis). Stocks tend to be valued on that basis. Also keep in mind there are clear winners in this environment, many of them in the e-commerce, consumer staples, healthcare, and technology areas.

So while earnings will likely be down significantly over the next couple of quarters, the crisis is temporary. We expect a strong second half rebound in corporate profits, bolstered by the massive fiscal and monetary stimulus that has been put in place. We believe the market is looking ahead to better days in 2021, which is a big reason why stocks are up so much over the past month.

Look for more on the earnings season in upcoming Weekly Market Commentaries and on our earnings season dashboard on the LPL Research blog.

IMPORTANT DISCLOSURES

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities. All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

This Research material was prepared by LPL Financial, LLC.

Securities and advisory services offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (Member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment advice from a separately registered independent investment advisor that is not an LPL affiliate, please note LPL makes no representation with respect to such entity.

- Not Insured by FDIC/NCUA or Any Other Government Agency

- Not Bank/Credit Union Guaranteed

- Not Bank/Credit Union Deposits or Obligations

- May Lose Value

For Public Use | Tracking # 1-05002655