Tip: Still Selling Strong. In 2017, investors purchased $192.1 billion in annuity contracts. Most of this capital—$108 billion—went into fixed annuities.

Source: LIMRA, 2018

Individuals hold about $2.2 trillion in annuity contracts; a tidy sum considering an estimated $9.2 trillion is held in all types of IRAs.1

Annuity contracts are purchased from an insurance company. In exchange, the insurance company makes regular payments to the buyer — either immediately or at some date in the future. These payments can be made monthly, quarterly, annually, or as a single lump-sum. Annuity contract holders can opt to receive payments for the rest of their lives or for a set number of years.

The money invested in an annuity grows tax-deferred. When the money is withdrawn, the amount contributed to the annuity will not be taxed, but earnings will be taxed as regular income. There is no contribution limit for an annuity.

There are two main types of annuities.

Fixed annuities offer a guaranteed payout, usually a set dollar amount or a set percentage of the assets in the annuity.

Variable annuities offer the possibility to allocate premiums between various subaccounts. This gives annuity owners the ability to participate in the potentially higher returns these subaccounts have to offer. It also means that the annuity account may fluctuate in value.

Indexed annuities are specialized variable annuities. During the accumulation period, the rate of return is based on an index.

Fast Fact: Fine Print. Since variable annuities give you the option to allocate your premium between various subaccounts, it’s important to read the prospectus before you invest.

Annuities have contract limitations, fees, and charges, including account and administrative fees, underlying investment management fees, mortality and expense fees, and charges for optional benefits. Most annuities have surrender fees that are usually highest if you take out the money in the initial years of the annuity contact. Withdrawals and income payments are taxed as ordinary income. If a withdrawal is made prior to age 59½, a 10% federal income tax penalty may apply (unless an exception applies). The guarantees of an annuity contract depend on the issuing company’s claims-paying ability. Annuities are not guaranteed by the FDIC or any other government agency.

Variable annuities are sold by prospectus, which contains detailed information about investment objectives and risks, as well as charges and expenses. You are encouraged to read the prospectus carefully before you invest or send money to buy a variable annuity contract. The prospectus is available from the insurance company or from your financial professional. Variable annuity subaccounts will fluctuate in value based on market conditions, and may be worth more or less than the original amount invested when the annuity expires.

CASE STUDY: ROBERT’S FIXED ANNUITY

Robert is a 52-year-old business owner. He uses $100,000 to purchase a deferred fixed annuity contract with a 4% guaranteed return.

Over the next 15 years, the contract will accumulate tax deferred. By the time Robert is ready to retire, the contract should be worth just over $180,000.

At that point the contract will begin making annual payments of $13,250. Only $7,358 of each payment will be taxable; the rest will be considered a return of principal.

These payments will last the rest of Robert’s life. Assuming he lives to age 85, he’ll eventually receive over $265,000 in payments.

Robert’s annuity may have contract limitations, fees, and charges, including account and administrative fees, underlying investment management fees, mortality and expense fees, and charges for optional benefits. His annuity also may have surrender fees that would be highest if Robert took out the money in the initial years of the annuity contact. Robert’s withdrawals and income payments are taxed as ordinary income. If he makes a withdrawal prior to age 59½, a 10% federal income tax penalty may apply (unless an exception applies).

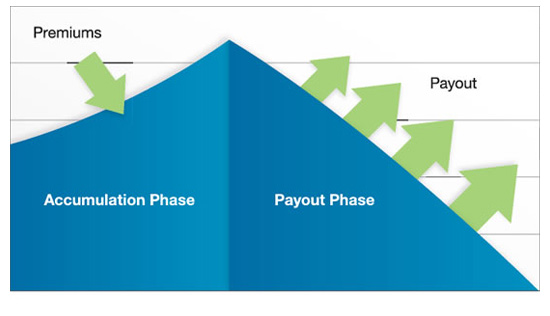

TWO PHASES

Deferred annuity contracts go through two distinct phases: accumulation and payout. During the accumulation phase, the account grows tax deferred. When it reaches the payout phase, it begins making regular payments to the contract owner — in this case annually.

- Investment Company Institute, 2018

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice. It may not be used for the purpose of avoiding any federal tax penalties. Please consult legal or tax professionals for specific information regarding your individual situation. This material was developed and produced by FMG Suite to provide information on a topic that may be of interest. FMG, LLC, is not affiliated with the named broker-dealer, state- or SEC-registered investment advisory firm. The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security. Copyright 2022 FMG Suite.