Parenthood can be both wonderfully rewarding and frighteningly challenging. Children give gifts only a parent can understand — from sticky-finger hugs to heartfelt pleas to tag along on Saturday morning errands. You raise them with a clear goal that you secretly dread will actually take place — that someday they will be grown, independent, and ready to move out on their own, and your work will be over.

As your children travel this long and never-dull road from infancy to adulthood, you try to protect them. You want to make sure that they are financially secure, but meeting expenses can be challenging. Fortunately, you can take steps to prepare for the financial challenges you face.

REASSESS YOUR BUDGET

As your family grows, you may need to make changes to your budget. Many living expenses may increase, including grocery, clothing, transportation, health-care, insurance, and housing costs. You may also need to account for new expenses, such as child care, or adjust your budget to account for a decrease in your income if you decide to become a stay-at-home parent. Your budget may also need to expand to include new financial goals, such as saving for college or buying a home.

Making sure that your budget reflects your new financial priorities can help you stay on track.

REVIEW YOUR LIFE INSURANCE COVERAGE

What would happen to your children if something happened to you? Life insurance is an effective way to protect your family from the uncertainty of premature death. It can help ensure that a preselected amount of money will be on hand to replace your income and help your family members — your children and your spouse — maintain their standard of living.

With life insurance, you can select an amount that will help your family meet living expenses, pay the mortgage, and even provide a college fund for your children. Best of all, life insurance proceeds are generally not taxable as income. Keep in mind, though, that the cost and availability of life insurance depend on factors such as age, health, and the type and amount of insurance purchased. As with most financial decisions, there are expenses associated with the purchase of life insurance.

CONSIDER PURCHASING DISABILITY INCOME INSURANCE

If you become disabled and unable to work, disability income insurance can pay benefits — a specific percentage of your income — so you can continue meeting your financial obligations until you are back on your feet.

What about Social Security? If you do become permanently and totally disabled and are unable to do work of any kind, you may be eligible for benefits, but qualifying isn’t easy. For more flexible and comprehensive protection, consider buying disability income insurance.

KEEP SAVING FOR RETIREMENT

Many well-intentioned parents put saving for retirement on hold while they save for their children’s college education. But if you do so, you’re potentially sacrificing your own financial well-being. If you postpone saving for retirement, you might miss out on years of tax-deferred growth, and it may be hard to catch up later. Ideally, you’ll want to save regularly for both goals, but if you have limited funds, prioritize saving for retirement. Your child may receive financial aid to pay for college, but there’s no such option for you.

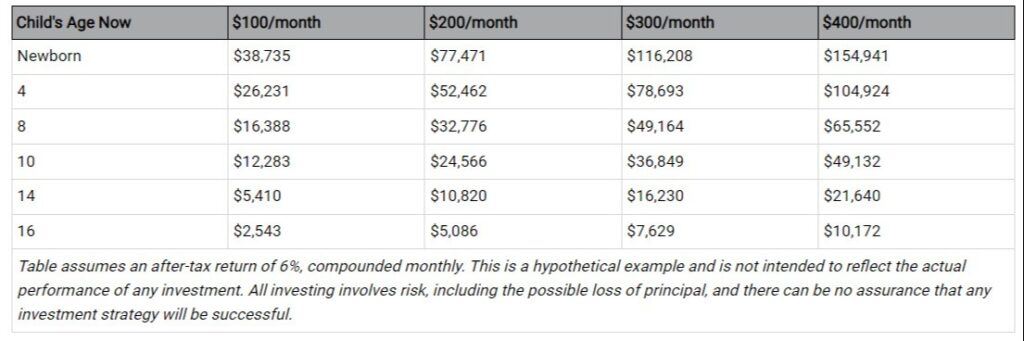

START BUILDING A COLLEGE FUND NOW

According to the College Board report, Trends in College Pricing and Student Aid 2021, for the 2021 – 2022 school year, the average cost for one year at a four-year public college is $27,330 (for in-state students), while the average cost for one year at a four-year private college is $55,880 (the total cost of attendance includes tuition and fees, room and board, books and supplies, transportation, and other miscellaneous costs). Even if those numbers don’t go up (and they are expected to continue increasing), that would come to $109,320 for a four-year degree at a public college, and $223,200 at a private university. Oh, and don’t forget graduate school.

College costs may seem daunting, especially if you’re still paying off your own college loans, but you have about 18 years before your newborn will be a college freshman.

By starting today, you can help your children become debt-free college grads. The secret is to save a little each month, take advantage of compounding, and have a sum waiting for you when your child is ready for college. The following chart shows how much money might be available for college when your child turns 18, if you save a certain amount each month.